Quote from Roman on July 17, 2024, 2:55 amHello everybody!

I'm trying to find the amount to pay-off by exploring a documents from a bank.

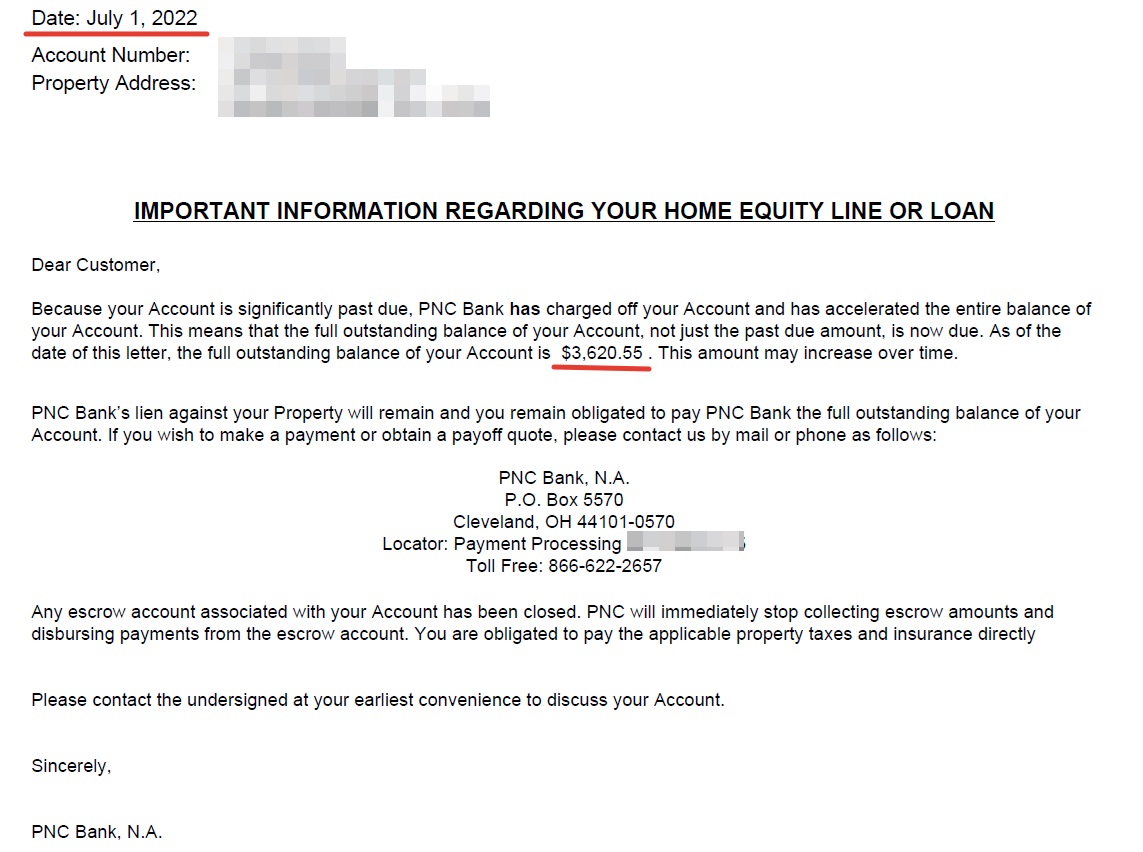

On July 1, 2022, the bank sent the borrower a demand to pay the full outstanding balance and indicated the amount: $3620.55

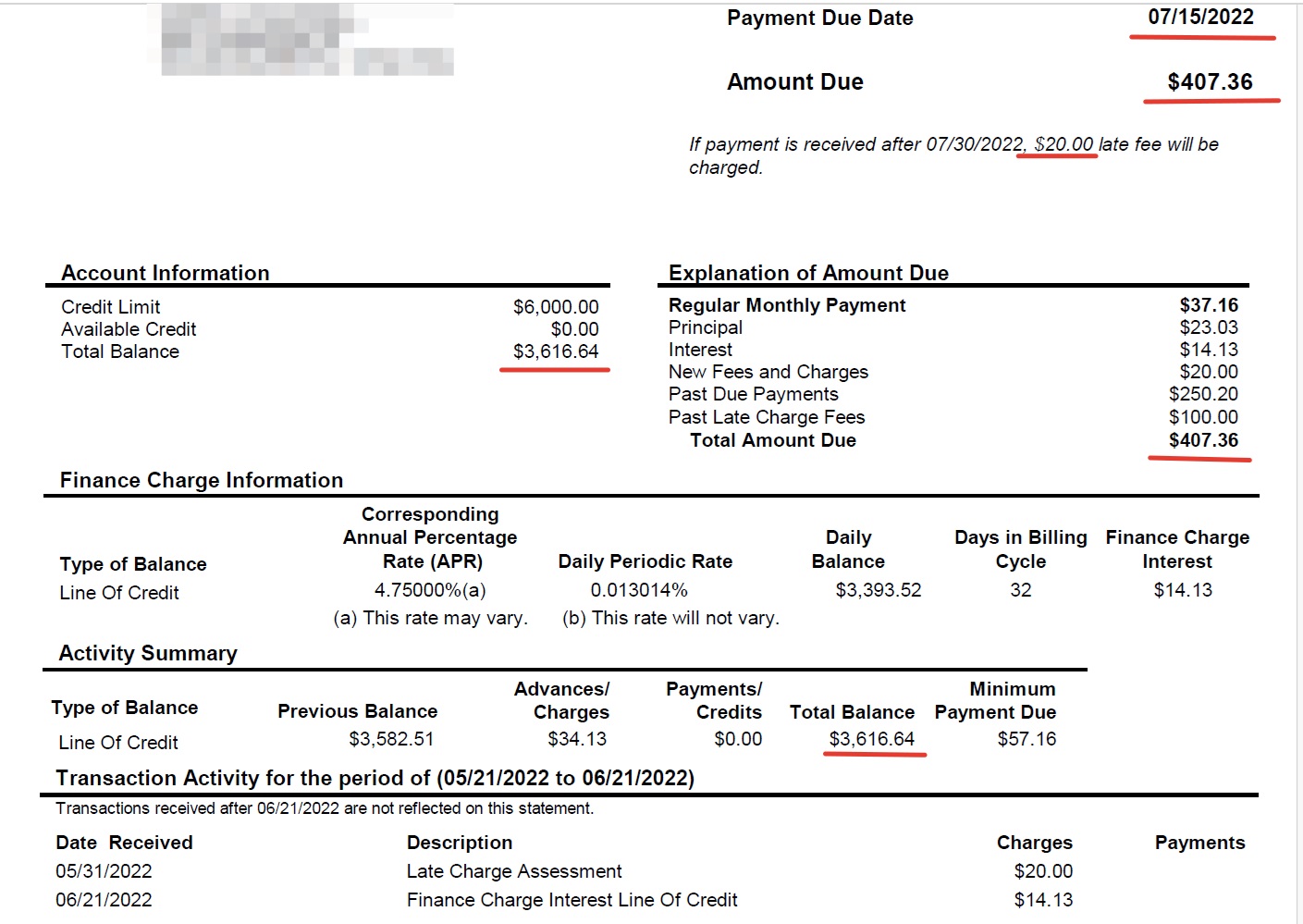

On July 15, 2022, the bank sent the borrower CONSUMER BILLING STATEMENTS, which indicated both the total amount of the balance and the Total Amount Due.

I didn’t find the amount $3620.55 in CONSUMER BILLING STATEMENTS. How can someone understand from these two documents what the total amount to be paid is?

Is it $407.36 (Total Amount Due) + $20.00 (late fee) + $3,616.64 (Total Balance) = $4,044.00 ?

or just $20.00 (late fee) + $3,616.64 (Total Balance) = $3,636.64 ?

or $3,620.55 (outstanding balance on 1st of July) ?Thank you for your attention!

Hello everybody!

I'm trying to find the amount to pay-off by exploring a documents from a bank.

On July 1, 2022, the bank sent the borrower a demand to pay the full outstanding balance and indicated the amount: $3620.55

On July 15, 2022, the bank sent the borrower CONSUMER BILLING STATEMENTS, which indicated both the total amount of the balance and the Total Amount Due.

I didn’t find the amount $3620.55 in CONSUMER BILLING STATEMENTS. How can someone understand from these two documents what the total amount to be paid is?

Is it $407.36 (Total Amount Due) + $20.00 (late fee) + $3,616.64 (Total Balance) = $4,044.00 ?

or just $20.00 (late fee) + $3,616.64 (Total Balance) = $3,636.64 ?

or $3,620.55 (outstanding balance on 1st of July) ?

Thank you for your attention!

Uploaded files:

Quote from jdarvill on July 18, 2024, 1:12 pmI'll take a crack at this. Interest is typically compounded daily so the payoff amount changes every day. The billing statement appears to go through 6/21 and the charge off notice is dated 7/1 so that is likely the reason that the stated balances are slightly different.

A payoff statement has two key pieces of information: a payoff amount and a date that the payoff is good for. A payoff would also include any applicable legal fees, lender advances on taxes/insurance, etc., which aren't typically included on billing statements, plus all late fees and interest as of a given date.

Someone who knows more than me would have to chime in as to whether the charge off amount can include everything that would normally be included in a payoff statement such as allowable legal fees. It's possible that the charge off amount in the notice was the full payoff amount as of 7/1, but the current payoff amount may be higher if you include accrued interest and late fees since the date of the notice.

If all I had to go on were these docs and I know that no additional payments have been made, I would probably use the statement balance as of 6/21 from the billing statement plus interest since 6/21 and add late fees for any payments due and not received since 6/21. On the other hand, if monthly statements have not been generated since 6/21/22, I might also talk to a lawyer or servicer about whether there may be any issues with charging the additional fees since then. Not sure if there may be any locality-specific rules about that.

I'll take a crack at this. Interest is typically compounded daily so the payoff amount changes every day. The billing statement appears to go through 6/21 and the charge off notice is dated 7/1 so that is likely the reason that the stated balances are slightly different.

A payoff statement has two key pieces of information: a payoff amount and a date that the payoff is good for. A payoff would also include any applicable legal fees, lender advances on taxes/insurance, etc., which aren't typically included on billing statements, plus all late fees and interest as of a given date.

Someone who knows more than me would have to chime in as to whether the charge off amount can include everything that would normally be included in a payoff statement such as allowable legal fees. It's possible that the charge off amount in the notice was the full payoff amount as of 7/1, but the current payoff amount may be higher if you include accrued interest and late fees since the date of the notice.

If all I had to go on were these docs and I know that no additional payments have been made, I would probably use the statement balance as of 6/21 from the billing statement plus interest since 6/21 and add late fees for any payments due and not received since 6/21. On the other hand, if monthly statements have not been generated since 6/21/22, I might also talk to a lawyer or servicer about whether there may be any issues with charging the additional fees since then. Not sure if there may be any locality-specific rules about that.

Quote from Roman on July 18, 2024, 1:46 pmThanks @jdarvill for the answer! I understand that a lender has the right to request reimbursement from the borrower for all charges and additional costs for courts, lawyer, notary, etc.

But I had in mind the most general case: for instance I just received a Customer billing statement from the bank. Looking at it, is it possible to calculate how much I should pay one-time in order to cover not only all arrears to the lender, but also the unpaid principal balance? We are talking only about the data from this document, without including any unknown possible payments in the future.

I'm guessing UPB = $3,616.64 (total balance value)

In addition to UPB, what amount still needs to be paid? Obviously not Total Amount Due $407.36, since this value also includes the Principal part $23.03

I tried to find a clue on the PNC bank website and even found an approximately similar case, but there is no solution there:

https://www.pnc.com/en/customer-service/home-equity-customer-service/home-equity-line-of-credit-statement-overview.html

Thanks @jdarvill for the answer! I understand that a lender has the right to request reimbursement from the borrower for all charges and additional costs for courts, lawyer, notary, etc.

But I had in mind the most general case: for instance I just received a Customer billing statement from the bank. Looking at it, is it possible to calculate how much I should pay one-time in order to cover not only all arrears to the lender, but also the unpaid principal balance? We are talking only about the data from this document, without including any unknown possible payments in the future.

I'm guessing UPB = $3,616.64 (total balance value)

In addition to UPB, what amount still needs to be paid? Obviously not Total Amount Due $407.36, since this value also includes the Principal part $23.03

I tried to find a clue on the PNC bank website and even found an approximately similar case, but there is no solution there:

https://www.pnc.com/en/customer-service/home-equity-customer-service/home-equity-line-of-credit-statement-overview.html

Quote from jdarvill on July 18, 2024, 2:24 pmThe Total Amount Due is a reinstatement amount, which would make the account current as of the 7/15/22 due date. As you identified, that amount isn't particularly relevant in determining the payoff amount.

I think $3,616.64 is the amount you're looking for. Looking closely at this statement, I would guess that the Daily Balance (3,393.52) is the UPB, which they are using to calculate interest, and the Total Balance (3,616.64) is the UPB/Daily Balance plus accumulated late charges and accrued interest as of the end of the period, 6/21/22.

In other words, I believe 3,616.64 would have been the payoff amount to close the account as of 6/21/22 (the end of the statement period) with the caveat that there may still be an amount owed for allowable legal expenses, etc., that had already been incurred by PNC or any previous note holder that may not be included anywhere on the billing statement.

The Total Amount Due is a reinstatement amount, which would make the account current as of the 7/15/22 due date. As you identified, that amount isn't particularly relevant in determining the payoff amount.

I think $3,616.64 is the amount you're looking for. Looking closely at this statement, I would guess that the Daily Balance (3,393.52) is the UPB, which they are using to calculate interest, and the Total Balance (3,616.64) is the UPB/Daily Balance plus accumulated late charges and accrued interest as of the end of the period, 6/21/22.

In other words, I believe 3,616.64 would have been the payoff amount to close the account as of 6/21/22 (the end of the statement period) with the caveat that there may still be an amount owed for allowable legal expenses, etc., that had already been incurred by PNC or any previous note holder that may not be included anywhere on the billing statement.

Quote from Roman on July 18, 2024, 2:44 pmThe difference between Total Balance and Daily Balance is $223.12 and I cannot calculate this value from the components of the Total Amount Due components, so this guess needs to be improved.

I also think that demanding payment of the Total Balance as of June 21 is quite logical, and, having an updated pay-off value as of July 1 (from the letter), which also informs about the charge-off of the account (which means further accrual of interest is risky) , I will demand this updated amount from the borrower for payment.

The difference between Total Balance and Daily Balance is $223.12 and I cannot calculate this value from the components of the Total Amount Due components, so this guess needs to be improved.

I also think that demanding payment of the Total Balance as of June 21 is quite logical, and, having an updated pay-off value as of July 1 (from the letter), which also informs about the charge-off of the account (which means further accrual of interest is risky) , I will demand this updated amount from the borrower for payment.